If Your Products Can't Quote in Seconds, You're Not in the Queue

Last September, when OpenAI and Stripe launched the Agentic Commerce Protocol, the reaction in commerce was immediate. ChatGPT users could buy from Etsy sellers directly in the chat window, without a redirect or a separate checkout page. Merchants indexed into ACP-compatible infrastructure would surface in those transactions. Merchants who hadn't simply wouldn't appear.

Six months later, OpenAI retired Instant Checkout. Amazon blocked ACP crawlers entirely, removing 600 million products from ChatGPT results. There are now ten competing agentic commerce protocols in the market, with no consolidation in sight.

That sequence isn't evidence that the concept failed. It's the market working through the plumbing: payment models, trust frameworks, attribution, protocol standardization. That work is underway, and when it resolves, the routing logic will be the same as it was on day one: products that are machine-readable surface, and products that aren't indexed return nothing.

Insurance is next in line for this transition, and the infrastructure question is identical.

Nobody's calling it discrimination, because no protocol penalizes anyone. They route to whoever is ready.

The routing logic doesn't negotiate

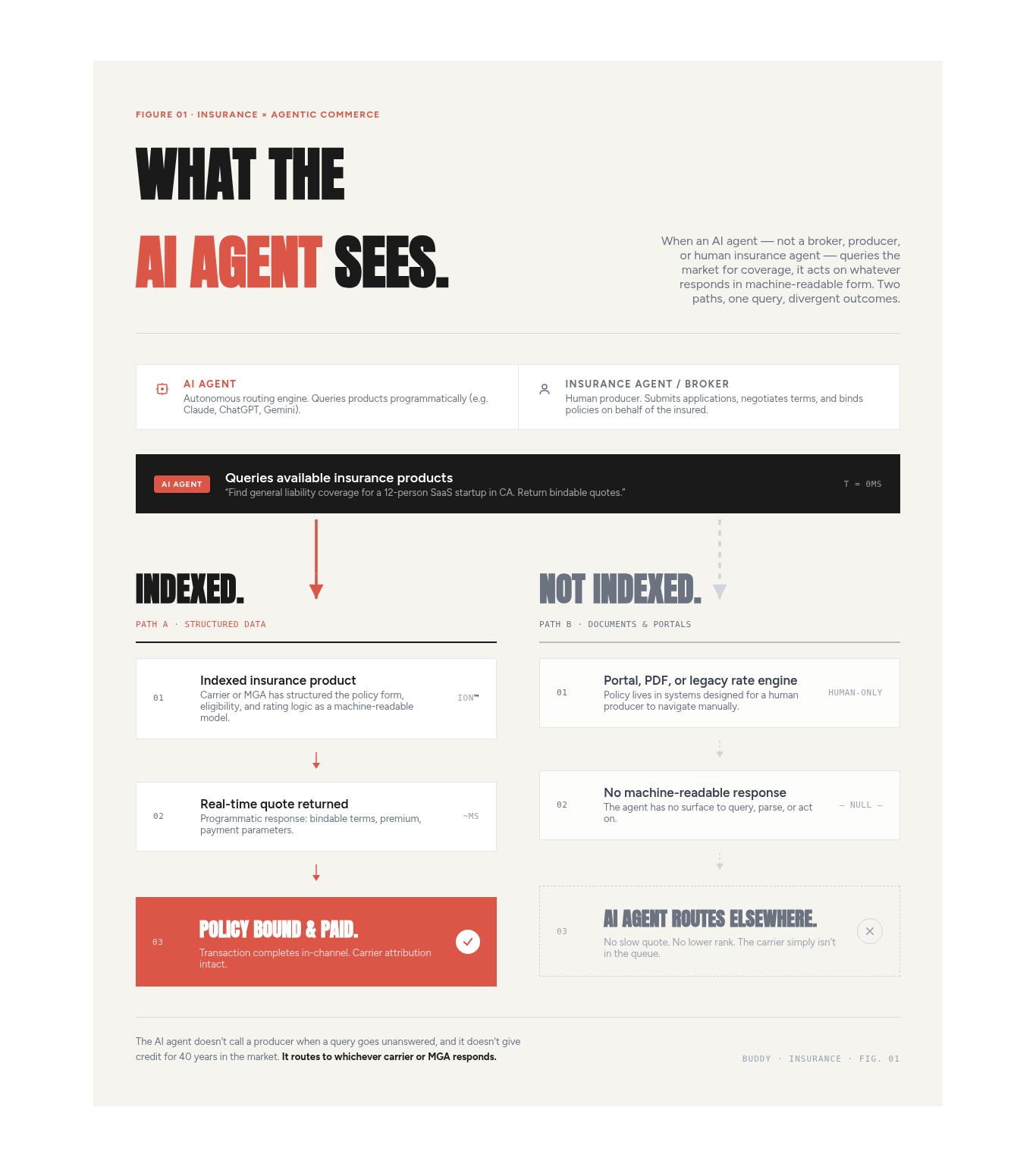

When an AI agent handles a transaction, the decision logic is mechanical, not relational. The agent queries for available products that match the buyer's parameters. It gets machine-readable responses back, or it doesn't. Products that are structured data return a quote. Products that live in PDFs, portals, or legacy rate engines return nothing the agent can act on.

The agent doesn't call a producer when a query goes unanswered, and it doesn't give credit for 40 years in the market or recognize the brand. It routes to whoever responds.

This is already happening in retail. It will happen in insurance. Your products will be queried by AI agents. The only question is whether they'll respond.

Who actually controls the speed

Brokers can't fix this. Quote speed is a function of the underwriting engine, and brokers don't own the underwriting engine. They can streamline submissions. They can reduce friction on their side of the transaction. But they can't make a carrier's product return a real-time, machine-readable quote if the infrastructure isn't built to do that.

Carriers can. MGAs with binding authority can. They control the rating engine. They decide whether their products are indexed as structured data that can be queried at machine speed, or whether they remain locked in systems designed for human navigation.

That's the lever. It belongs to carriers and MGAs, not to distribution.

What "not in the queue" actually looks like

An AI agent receives a request: find coverage for X, return options. It queries the products it has access to. Indexed products, the ones that exist as structured data with a machine-readable interface, return quotes in milliseconds. The agent evaluates them, ranks them, and presents options or completes the transaction. Products that aren't indexed don't return a slow response or a lower-ranked one. They return nothing, and the agent moves on to whatever it can reach.

The analogy from retail holds: if your product isn't in the catalog, it doesn't show up in search. The catalog isn't the storefront. It's the prerequisite. Being good at what you do doesn't matter if you're not findable.

The infrastructure behind the speed

The real issue is whether your products are structured data or static documents.

Products that exist as structured data — a machine-readable model of coverage terms, eligibility rules, pricing logic, and payment parameters — can be queried, quoted, and bound programmatically. Products that exist as PDFs, fillable forms, or portal workflows require a human in the loop at every step. AI agents don't have a loop for that.

The work isn't in AI strategy or chatbot RFPs. It's in whether the product itself is machine-readable.

At Buddy, we index insurance products as structured data. From that index, products distribute across Offer Elements for human commerce and Buddy MCP for AI commerce, without a separate integration build for each channel. Index once, distribute everywhere.

That's where Buddy MCP comes in. It makes indexed products natively accessible to AI agents for querying, quoting, binding, and payment — full transaction capability, not just information retrieval. Products indexed in Buddy's platform are AI-agent-ready from the moment of indexing. When the routing protocols in insurance catch up to what's already live in retail, those products will be in the queue. The ones that aren't indexed won't.

The carriers who moved early on ACP-compatible infrastructure in retail didn't have to scramble when ChatGPT started processing purchases. They'd already done the indexing work. The carriers and MGAs who index now won't have to scramble when agentic routing goes live in insurance distribution.

What to do now

Three questions worth sitting with:

- Are your products structured data, or documents and portals? Policy forms, eligibility rules, and rating logic that live as machine-readable models can be queried programmatically. PDFs and portal workflows can't.

- Can your rating engine respond to a programmatic query in real time, or only to a browser session? If a quote requires a human to navigate a screen, an AI agent can't get one.

- Does your distribution infrastructure span both human and AI channels from the same index, or would an AI channel require a separate build? Separate builds mean you're always one protocol behind.

If you're not sure where you stand on any of those, that's the place to start.

We work with carriers and MGAs on this. If you want to walk through where your products sit relative to what's coming, get in touch.

Buddy is a digital commerce platform for insurance. Index once, distribute everywhere.